Market Comments: Q1 2026

April 2026

Entering the year, expectations for continued economic growth, strong corporate earnings, and relatively tame inflation were widespread. Though that sentiment remains largely intact, uncertainty related to the Iran war has investors reassessing their risk appetite. All global stock market indices turned sharply lower at quarter-end.

In the U.S., the Dow Jones Industrial Average, the Standard & Poor’s 500 Index, and the NASDAQ Composite Index returned -5.2%, -5.0%, and -4.7%, respectively, in March. International stocks fared worse, with the MSCI EAFE Index and MSCI Emerging Markets Index returning -10.2% and -13.0%, respectively.

Through the first three months of the year, the Dow, the S&P 500, and the NASDAQ returned -3.2%, -4.4%, and -7.0%, respectively, while the MSCI EAFE and Emerging Markets indices returned -1.1% and -0.1%, respectively.

Benchmark S&P 500 results over the period were the worst since 2022, when the index ended the year down nearly 18%.

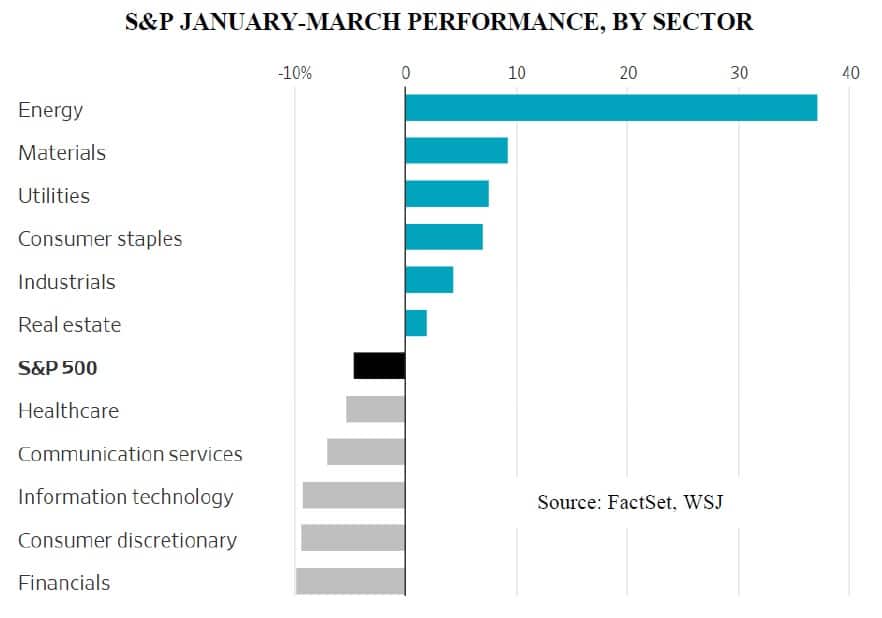

The favored sectors of the last few years, those that hold all the Mag 7 stocks – communication services, information technology, consumer discretion – were among the worst performers as AI-driven business model disruption risk accelerated. Only the financial sector had lower returns in the quarter.

Oil prices spiked over the period following the capture of Venezuelan leader Maduro in January and the U.S.-Israel airstrikes in March. It is of little surprise that energy stocks were the front runners in the quarter, returning nearly 40%.

Damage to energy facilities in the Middle East, coupled with Iran’s retaliatory efforts across the region, caused the flow of oil through the Strait of Hormuz to all but cease. The Strait is the chokepoint for around 20% of the 100 million barrel a day oil market. At present, the scope of potential outcomes to energy markets is wide and unknown, as investors attempt to digest the potential length and severity of further supply chain disruptions, which are the highest in history.

Interest rates, which declined slightly through the first two months of the year, reversed course after the conflict began. The benchmark 10-year Treasury, which began 2026 at 4.18%, ended February yielding 3.97%. At quarter-end, with commodity prices spiking and inflation expectations growing, the yield on the benchmark 10-year Treasury rose to 4.30%.

Through February (latest data available), inflation (CPI) remained steady at 2.4%, year over year. Given higher energy prices in March, the February reading is broadly viewed as a new baseline, with expectations for price pressure over the coming months. Since the energy component is less than 6.5% of the CPI calculation, a sudden inflation spike is unlikely. Core inflation, which strips out the food and energy components, was also steady at 2.5%, year over year through February.

Following a lousy February employment report showing the U.S. economy lost a net 133,000 jobs, there was a strong rebound of 178,000 new jobs created in March. Gains were most notable in healthcare (+76,000) following the end of a widespread hospital strike, while milder weather helped the leisure & hospitality (+44,000) and construction (+26,000) industries. Federal government employment declined by 18,000 for the month. The federal government now employees 352,000 fewer people than in January of last year.

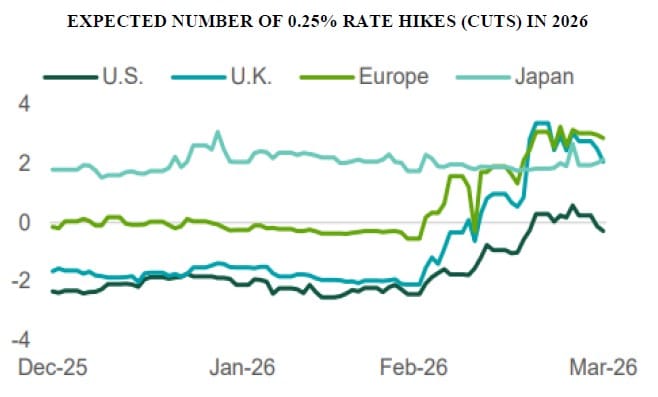

The Federal Reserve made no rate adjustments in the first quarter after three consecutive 0.25% cuts to end 2025. However, investor expectations for future central bank activity shifted significantly after the start of the war.

Shifts in sentiment were felt globally. Other than at the Bank of Japan, expectations (futures) suggest central banks will take a more hawkish stance on monetary policy in 2026 to offset expected inflation.

Probabilities for rate changes in 2026 at the European Central Bank and the Bank of England swung from no change and two 0.25% rate cuts, respectively, at the start of the year, to now three rate hikes (each) by year-end.

Fed funds futures in the U.S., which forecasted two 0.25% rate cuts at the start of the year, now predict no adjustments will occur in 2026.

Earnings season will begin in the coming days, as investors seek clarity on the impact global uncertainty will have on financial markets and, more broadly, economic conditions. The U.S. is a major oil producer and net-exporter, which insulates it from the energy shortages many countries are experiencing.

However, because oil is sold on a global market, higher prices are disrupting some U.S. consumer segments. According to Urban Institute data, delinquency rates on credit cards for low- and medium-income borrowers are now higher than their pre-pandemic peak.

Last year, upper-income households helped sustain consumer spending, the key driver of the U.S. economy. Further declines in stock prices could disrupt spending patterns of even the wealthiest consumers, while higher gas prices for a prolonged period may add to the strain being felt by the other segments of the population.

To be clear, the probability of a recession occurring in the coming months is low, and wars and other geopolitical shocks typically do not have lasting negative implications on stocks. Investing with prudence, which involves preparing for known short-term liquidity needs whether conditions are stable or otherwise, also necessitates discipline and, often, patience.

Earnings forecasts for 2026 are higher today than at the start of year. While there is no assurance that increased earnings growth will translate into better market conditions in the short term, we remain committed to following our long-term investment discipline and taking advantage of opportunities during those inevitable periods of market disruption.

Start planning for a stronger financial future.

Let us help you build a tailored plan that will help you achieve your financial goals.

Find an Advisor